Do you have pressing questions?

Submit them to us on Instagram. We are working to personally message back all the pros that reach out.

Read time: 30 minutes

(Note: If you prefer to watch a video on this topic, click here to watch the Federal Stimulus webinar with our friends at Rising Tide Society and HoneyBook.)

Taking on this Stimulus Bill conversation is a HUGE undertaking. So before we jump into all the pieces of the CARES Act, we wanted to set the groundwork a bit.

We build partnerships at TAG. So we have a really big network of accountants, lawyers, financial advisors that help our members. So we have interviewed many of these partners. Also at the Abundance Group, our team researched basically non-stop since the March 27th when this bill was signed.

The ace in our pocket has been Matt Mohning with MSM Financial. Not only is he our personal account for both companies (Ashley also owns a large planning company) BUT he was a policy advisor to the Chairman of the U.S. Senate Budget Committee in Washington, D.C for a very long time. So he understands both the political and financial sides of this topic. And YES he READ THE BILL. So he was a huge asset as we built out this resource for you all!

So let’s kick it off. First we need to talk at the 10,000 Foot Level:

- Everything happened extraordinarily fast (days, not months or years)

- Because of this they are using current institutions (State unemployment offices, SBA approved banks, IRS systems) as funnels, to get the cash to the public as soon as possible.

- From the standpoint of the CARES Act, it's groundbreaking in two ways:

- How much it gives (Over $2 Trillion Dollars), and

- How fast it got done (Again, in days, not months/years)

We’ve heard analysis of “it’s like ready, shoot, aim.” And I couldn’t agree more.

So they created the policy, and now they have to build the procedures, so it’s backwards from standard practice. So it’s completely expected to be confusing. Even the institutions they are leveraging are STILL awaiting guidance.

The night before funding was set to go live, the US Treasury finally released information to the public as well as the banks themselves on filing for SBA loans and Paycheck Protection Program. So to say it’s happening in live time is an understatement!

Our team at The Abundance Group knows how impactful this bill will be for businesses, a lifeline to save many of them, so we want to mention we are literally on the very front lines. Learning as much as we can, as fast as we can. But we want to make it clear that things are absolutely changing every single day.

We are doing all we can to get any and all the CREDIBLE information to you we can. Procedures will be updating, so you should expect them to change and vary state by state. But we are here to give you the very best information we possibly can.

With that, let’s jump into the main topics along with some of the most frequently asked questions we have received over the last few weeks.

There will be four main sections: Stimulus Checks, Unemployment, Paycheck Protection Program, and SBA Loans/Grants. We have given as much information as we can on each topic, and have addressed the most asked questions for each section. So feel free to skip to the topic you are most interested in learning more about.

Note: After we cover the bill and its programs that can benefit you, we also include a number of additional resources in the areas of Cashflow, Marketing, Legal and FREE STUFF!

_________________________________________________________________

Stimulus Checks:

Can you give us a brief overview of the stimulus checks—who is getting them? How much money does each person get? When should we expect to receive them?

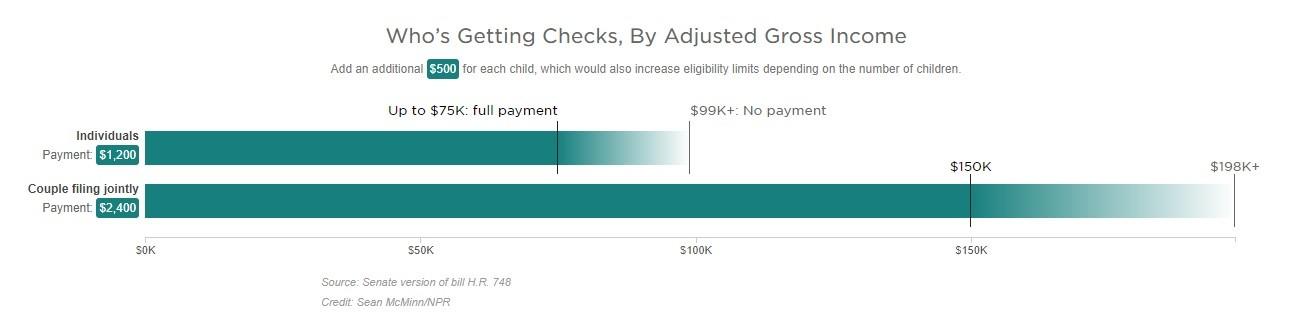

- Taxpayers will receive rebate checks of $1,200 per adult and $500 per child under 17 years old. Eligibility is limited based on income. Full rebate checks will go to taxpayers with Adjusted Gross Income (AGI) up to: Single: $75,000, Married filing Jointly: $150,000, Head of Household: $112,500. The rebate is reduced by 5% of the amount of income that exceeds the AGI limit. The Treasury set a goal of starting to issue rebate checks within three weeks (the bill passed on 3/27)-- this MIGHT be ambitious, just to set some expectations.

Do these have to be paid back?

- No, the rebates don’t need to be paid back.

Are they recurring or one time?

- The rebate is a one-time payment of the maximum amount eligible to receive. There are two opportunities to receive the funds. The rebate checks will go out in the next several weeks. Eligibility is based on 2019 (or 2018) income. Those who didn’t qualify based on 2019 income, but do qualify based on 2020 income will receive their rebate or the higher amount they were due to receive when they file their 2020 tax return.

Here is a great visual that was really helpful to see what this looks like:

Found via NRP- this link: Source: Senate version of bill H.R. 748 Credit: Sean McMinn/NPR

_________________________________________________________________

Employment (& Unemployment):

Who is eligible for unemployment? Does this include self employed people and independent contractors?

Under the new plan, you would be eligible if you meet any of the conditions below:

- You are self employed or part time and lost work due to a coronavirus reason

- You received a COVID-19 diagnosis, are experiencing symptoms, seeking a diagnosis or caring for a member of your family/household who received a diagnosis AND you’re unemployed, partly unemployed or cannot work as a result

- You rely on a facility, daycare or school to care for a child or other family member so you can work, and that facility has closed due to coronavirus

- You must self-quarantine on the advice of a healthcare provider because of exposure to coronavirus

- You are unable to get to work because of an imposed quarantine

- You were about to start a new job but can’t get there now because of an outbreak

- You were immediately laid off from a job and don’t have enough work history to qualify for benefits under normal conditions

- You are unemployed, partly unemployed or unable to work because your employer shut down your workplace

Who is not included in the bill?

- Workers who are able to work from home (This seems to reference corporate workers and not self-employed or part-time workers who work from home.)

- Those receiving paid sick leave or paid family leave

- New entrants to the workforce who cannot find jobs

- People who quit (or want to quit) because they are afraid of being at greater risk of contracting coronavirus if they continue to work

How much money do you receive in unemployment benefits?

- Depends on which state you live in and would be calculated based on your previous income.

- Additionally, eligible workers would get an extra $600 per week from the federal government on top of their state’s weekly benefit.

- So for example, the weekly benefit in California is a maximum of $450. With the additional $600 from the federal government, eligible Californians could receive self employed unemployment benefits up to $1050 each week.

- States can send the payment in two separate payments or in one payment, but it must be paid weekly.

How long do you get unemployment?

- This also varies by state. Most states provide benefits for 26 weeks, although some provide benefits for less. The new bill adds an additional 13 weeks for all eligible workers. 39 weeks is the maximum time eligible workers can receive benefits, but this may be less depending on the state.

- The extra $600 payment would last for up to four months and cover weeks of unemployment ending July 31.

How long does the extended unemployment program last?

- The extended program would be open to workers who were newly eligible for unemployment benefits starting Jan. 27, 2020

How do I apply?

- Unemployment benefits will be administered by your state’s unemployment offices. To Apply, find your state here and click on the link to apply with your state’s office. Or for more information about filing for self employed unemployment benefits, check this unemployment benefits finder.

Additional Questions:

If I am still making some money from deposits for weddings will I still be able to file for unemployment?

- You may be eligible for a reduced benefit.

I visited our state’s site and it says unemployment benefits are not available for self-employed. Is this be true?

- The CARES Act extended unemployment to self-employed individuals. This law passed on 3/27/20. States are in the process of implementing this program. (So be sure to check again.)

- This was on careeronestop.org: "States are in the process of implementing these new rules and may not have updated information immediately. If you are out of work or have had your hours reduced you should continue to follow your state’s guidelines for filing for unemployment. Many states are experiencing extensive traffic and asking filers to be patient and persistent."

If weddings are not being canceled, but being postponed for the fall or next year, does that still count as unemployment?

- The likely answer is yes. We are still waiting for states to issue guidance on what counts as unemployment for self-employed individuals.

_________________________________________________________________

Paycheck Protection Program:

This is information pulled directly from the US Treasury Site, to ensure we are stating exactly what the program outlines.

Fully Forgiven: When used for Payroll costs, interest on (business) mortgages, rent, and utilities. (Due to likely high subscription, at least 75% of the forgiven amount must have been used for payroll). Loan payments will also be deferred for six months. No collateral or personal guarantees are required. Neither the government nor lenders will charge small businesses any fee. The amount os 2.5 times your average monthly payroll. (For examlpe, if you average monthly payroll is$10,000 - your max benefit would be $25,000.)

Must Be Kept on Payroll (or Rehire FAST!): Forgiveness is based on the employer maintaining or quickly rehiring employees and maintaining salary levels. Forgiveness will be reduced if full-time headcount declines, or if salaries and wages decrease. (High Level: 75% hired back, then 75% will be forgiven)

All Small Businesses Eligible: Businesses with 500 or fewer employees—including nonprofits, veterans organizations, tribal concerns, self-employed individuals, sole proprietorships, and independent contractors—are eligible.

When to Apply: Starting April 3, 2020, small businesses and sole proprietorships can apply. Starting April 10, 2020, independent contractors and self-employed individuals can apply. We encourage you to apply as quickly as you can, because there is a funding cap.

How to Apply: You can apply through any existing SBA 7(a) lender or through any federally insured depository institution, federally insured credit union, and Farm Credit System institution that is participating. Other regulated lenders will be available to make these loans once they are approved and enrolled in the program. You should consult with your local lender as to whether it is participating. All loans will have the same terms regardless of lender or borrower. A list of participating lenders as well as additional information and full terms can be found at www.sba.gov.

Here is the current PPP application:

https://www.sba.gov/sites/default/files/2020-04/PPP%20Borrower%20Application%20Form.pdf

Biggest questions we get around this is:

What if you don’t run actual payroll? You are a sole proprietorship or independent contractor. How do I know what qualifies as “payroll costs?”:

- Here is the very best resource (again, linked the US Treasury themselves where they state):

What counts as payroll costs? Payroll costs include:

- Salary, wages, commissions, or tips (capped at $100,000 on an annualized basis for each employee)

- Employee benefits including costs for vacation, parental, family, medical, or sick leave; allowance for separation or dismissal; payments required for the provisions of group health care benefits including insurance premiums; and payment of any retirement benefit

- State and local taxes assessed on compensation

- For a sole proprietor or independent contractor: wages, commissions, income, or net earnings from self-employment, capped at $100,000 on an annualized basis for each employee

_________________________________________________________________

SBA Loan & Grants:

SBA Disaster Loan Assistance: Who qualifies for these loans and what does loan forgiveness look like?

- It is important to point out that there is an SBA Disaster Loan and the new SBA Paycheck Protection Program. The SBA Disaster loan has to be paid back. The PPP will be forgiven, if used to pay wages, benefits, rent, mortgage payment, and utilities.

Who is eligible for these loans? LLC? Sole Proprietors?

- Businesses of all types (including sole-proprietors, self-employed individuals and independent contractors) are eligible

What is the interest rate and what are the pay back terms?

- SBA Disaster loans are max 30-year, 4% and not forgivable. The PPP (any unforgiven amount) interest rate is 0.5%, 2 year term, and again forgivable if conditions are met.

How do I sign up?

- You apply through an accredited SBA lender, mainly banks.

What Grant Programs are available?

- Emergency grants up to $10K - Small businesses may apply directly to the federal Small Business Administration to receive an economic injury disaster grant of up to $10,000 that does not need to be paid back. The money would be paid out to business owners within three days of their application's submission. It can be used to maintain payroll, cover paid sick leave and service other debt obligations. Used for fast cash, and it would be deducted if later apply for PPP. (Can’t double dip.)

What about those who are the sole employee. Do we qualify for the grant?

- Yes

Are there any negative future consequences for accepting the $10k SBA advance grant?

- No.

Do you know if credit score/history will affect this?

- No, it should not.

How to apply? https://covid19relief.sba.gov/#/

Here is a link to the SBA site for more information: https://www.sba.gov/funding-programs/loans/coronavirus-relief-options/economic-injury-disaster-loan-emergency-advance

If you are a small business, and if you are here reading this we assume you are,

THE MOST IMPORTANT PIECE is of the ENTIRE CARES Act is the following:

I am a S Corp business owner and just applied for unemployment last week. Do I still qualify for the SBA disaster loan? Do I need to cancel/withdraw my unemployment application?

- You would want to compare the two options and determine the best one for you. As an S-corp owner you have wages and profits. The expanded definition of unemployment may benefit you. However, the PPP loan to grant program is also a good option and may give you a higher benefit.

- And again, as a reminder, this does NOT just apply to S-Corps. If you are a sole proprietorship, or independent contractor as well, you NEED TO WORK YOUR OWN PERSONAL NUMBERS.

Our goal with this resource is to have you stop and do the math on what will work best for you business during this difficult season.

We want you to be protected.

We want the coming years to be the very best in your business.

A few closing tips:

- Watch for scams. You are all savvy business owners, but we know that there will be many people trying to take advantage of the situation. So just double check the credibility of any sources that you are trusting during this time. (Ashley has already had two text messages of companies try to get information from her. Just be smart!)

- Work closely with an accountant. Some are working directly with these programs to receive fees through the program itself, and have no cost to the business owner. Our accountant MSM financial works with businesses from all over the country. Here is Matt’s Contact Page: https://www.msmfinancial.com/

- Struggling getting your loan request submitted? This is something we are hearing a lot with our community. Working with larger banks that aren’t moving the needle in the way that wedding pros are needing. A quick tip we have is to talk with a local small business bank to see how they can help you. Having a personal relationship with a banker that you know and can call can make a huge difference!

- If we didn’t get to your question here, our team at The Abundance Group is committed to help, so please connect with us on IG.

We are here to help you. We love our community of wedding professionals and we know how devastating this has been for your 2020 wedding season already. We want to help you get through this as fast as we can.

Knowledge is power, and you are seeking answers. That is the first and MOST important step. Please let our team know how we can support you from here.

-Ashley, Dale and the Entire TAG Team

Beyond our recap of the Stimulus Bill, we wanted to get all our COVID resources in front of you.

So below are some of the most valuable pieces of content we have found. These range from more on the Bill to marketing, legal, and client management.

Pick and choose but know these were built by some of the smartest in their field, and we encourage you to continue your learning!

Financial/Stimulus (CARES Act)/Economic Relief Resources:

Below are a collection of the most CREDIBLE and helpful resources we have found when navigating the Stimulus Bill.

Overall Stimulus Bill Information:

Our incredibly helpful accountant: Matthew Mohning (MSM Financial) put together a brief overview and high level view of everything. GREAT place to get started in learning about the financial side of what you can be doing right now: https://www.msmfinancial.com/resources

Other Helpful Links (General Overview of Stimulus)

NY Times: https://www.nytimes.com/article/coronavirus-stimulus-package-questions-answers.html

NY Times: https://www.nytimes.com/2020/03/26/business/coronavirus-stimulus-small-business.html

Senator Rubio’s Post: (one if the biggest voices for Small Businesses)

https://www.rubio.senate.gov/public/_cache/files/28e8263e-e7d4-4da7-a67b-077c54ba4220/9F7B494B2E355791B24536DC2162CF16.final-one-pager-keeping-american-workers-paid-and-employed-act-.pdf

NPR: (with great visuals and breakdowns)

https://www.npr.org/2020/03/26/821457551/whats-inside-the-senate-s-2-trillion-coronavirus-aid-package

Paycheck Protection Program:

Overview of Paycheck Protection Program from US Treasury:

https://home.treasury.gov/system/files/136/PPP%20--%20Overview.pdf

This link includes answers to THE BIGGEST question that we received, what is included as “payroll costs” for sole proprietors or independent contractors.

Paycheck Protection Program for Borrowers from US Treasury:

https://home.treasury.gov/system/files/136/PPP--Fact-Sheet.pdf

Other Financial Resources:

The Abundance Group's Cashflow Strategies: www.theabundance.goup/cashflow

Ashley Ebert FB Live: How Simply Elegant is Working Through COVID (March 16h)

Ashley Ebert FB Live: Cash-flow Strategies you can do RIGHT NOW! (March 17th)

(Both of these are still EXTREMELY relevant on how you can protect your business on your own terms. If you are NOT looking for funding, but would rather self fund through this crisis, these are great Lives to watch!)

To view these videos, you will need to join the group if you are not already a member:

https://www.facebook.com/groups/weddingprosguidetoabundance/

HoneyBook Blog: Stimulus Package and Finances

https://www.honeybook.com/risingtide/self-employed-unemployment-coronavirus-stimulus-package

HoneyBook Financial Resources:

https://www.honeybook.com/risingtide/small-business-relief

Marketing:

Overall Marketing:

Should You Market Your Business Right Now?

https://www.taylrd.co/blog/should-you-market-your-business-right-now

What to Share on Social Media During Coronavirus:

https://www.taylrd.co/blog/what-to-share-on-social-media-during-coronavirus

Three Ways to Market Your Business:

https://www.chanceycharmweddings.com/three-ways-to-market-you-wedding-planning-business-during-coronavirus/

Blogging Advice:

Simple Tips for Better Blog Writing – Elisabeth Kramer:

https://www.photographersedit.com/blog/better-blog-writing/

Facebook Ads:

Join Katelin’s Group: https://www.facebook.com/groups/bookweddingsnow

Then you can view her AMAZING video on The Simplest Way To Set Up A FB + IG Ads:

https://www.facebook.com/katelinmarie.fas/videos/10158038894195359

Pinterest Training:

https://vanessakynes.com/signup-for-pinterest-training/

FREE Stuff:

FREE Email Templates for Communicating with your Couples (Partnership with Kayla Hollatz)

Access by dropping your email here: www.theabundance.group/cashflow

Three months of advertising with love Inc Magazine:

https://loveincmag.com/screw-covid-19-offering-3-months-free-advertising-wedding-pros/

Three month free trial for Pops of Pretty!

https://popsofpretty.memberspace.com/member/plans/0a06a93768

Stock Photos to Market Your Wedding Business: (with 10 Free Images)

https://www.sourcedco.com/blog/stock-photos-to-market-your-wedding-business

Coaching Sessions with Kyle Goldie: Join his Facebook Group to learn more! https://www.facebook.com/groups/rockstargrowth/

Coloring Sheets! (Because sometimes we just need to be able to chill out!) https://www.sourcedco.com/stock-art-graphics/free-coloring-pages-for-kids-and-grown-ups

Legal Information:

Postponement Agreement: https://blog.engagedlegal.com/blog/wedding-and-event-cancellation-covid

Engaged Legal also has a great Postponement Template:

https://www.engagedlegal.com/products/emergency-postponement-amendment-for-wedding-event-pros

A Q/A with Caroline Fox of Engaged Legal with Host Lauren Grove:

https://www.facebook.com/ELDForPros/videos/839448729869929/

GREAT General Information:

What to Do During this Pandemic: 90 Minute Video (within Kyle Goldie’s Facebook Group.)

https://www.facebook.com/groups/rockstargrowth/

When Business Slows Down:

https://www.photographersedit.com/blog/business-slows-down/

How to Serve Your Clients Amidst Fearful Times – Taylor Ford:

https://www.photographersedit.com/blog/fearful-times/

Get Ahead During Slow Season – Mike Morby:

https://www.photographersedit.com/blog/slowseason/

Things to Help Your Couples Through COVID:

Multiple Ways to Help Your Couples Navigate this Time:

https://theeverylastdetail.com/coronavirus-wedding-resources/

Email Template for Couples:

https://theeverylastdetail.com/coronavirus-wedding-postponement-email-templates-to-send-to-guests/

We truly hope that these resources help you feel informed on how to move forward with your business! Our goal in providing all of this information is to show that even in the unexpected moments, there is always room to think in an abundant way that leads to innovation and stronger client relationships.

To help our fellow wedding pros, we have been recording multiple Facebook Live videos inside our free Facebook group, Wedding Pros Guide to Abundance. Come join us to talk more about business strategy and connect with a like-minded community who can give encouragement and advice during the pandemic.

Was this resource helpful? If so, it can probably help other pros you know too. Be sure to share with others in the wedding industry!

Please copy this link:

https://www.theabundance.group/COVID

And share on Facebook!!

About the Authors

Dale & Ashley

The Abundance Group

Together, Dale and Ashley are the dad/daughter duo behind the membership for wedding pros, helping you get the results you’ve been striving for in your wedding business. We provide education and support to help our wedding pros abundantly navigate and grow through any situation—yes, even the coronavirus pandemic!